Between a deluge of mostly bullish stock market Q1 earnings in the last month, positive Inflation CPI data last week and a continued overall fixation on how the Federal Reserve in the United States will respond to such macro-economic data, it’s needless to say we’re at a pivotal turning point in the current market cycle. Where we were a mere two years ago in uncertain waters with the FED raising rates, rampant increasing YoY Inflation data and uncertainty in the Bond market, the FED’s objective of a “Soft landing” in an attempt to cool inflation and restore growth to the markets has remained in the minds of traders. It’s important for the FED to achieve this objective because as we saw for the greater part of 2022, increased inflation and rising prices in the market created further uncertainty in the Bond market, causing a sharp selloff; consequently, leading to a sharp spike in yields and an inverted Yield Curve. This proceeded the following hawkish rate hiking cycle and sentiment from not just the FED, but also most western Central banks globally such as Australia.

Several factors contribute to the inflation rate, including supply chain disruptions, labor market conditions, and commodity prices. The persistence of high inflation can be attributed to lingering supply chain issues, elevated demand for goods and services post-pandemic, and geopolitical tensions affecting oil and food prices. Whilst all the above factors are true, it’s also not the whole story. Aggressively doveish monetary policy from the FED and most developed Central Banks around the world during the pandemic saw us cutting rates to all-time lows. In the FED’s case, this was even as low as a flat 0% for the Federal Funds rate, combined with a $700 Billion Quantitative Easing Program that sought to inject significant currency into the Treasury market, in an attempt to re-inflate the market and stave off a more severe crash due to the economic conditions wrought by the pandemic at the time. Since then, we’ve witnessed the 2021 Bull run in Cryptocurrency that created investing euphoria to unprecedented levels, birthing meme stock investing such as $GME (GameStop stock) and DOGE coin, and of course plotting BTC at a near $70,000 USD high at the time. It’s needed to say that this was unsustainable in the short to medium term as we welcomed a rise in interest rates to curb the inflation in the broader economy that came with such mania, a stark contrast to the Zero Interest Rate Policy (ZIRP) the FED aggressively pushed just a few years prior. Ultimately, all of this has culminated and landed us here where we are today, let’s take a deeper look.

The FED managed to raise their Federal Funds Rate to a current target of 5.25%-5.50%. During the period of hiking, we saw a correction in the broader financial markets globally during 2022, however coming out of this we’ve seen steady gains and reversing of price to the upside for nearly all market sectors; including Cryptocurrency. US Inflation naturally has come down since the continuous FED hiking cycle, of which the last rate hike of 25 basis points was in July of 2023 creating the Federal Funds rate target of 5.25%-5.50% we see today. The corresponding downtrend in CPI data that came along with the hikes alleviated bearish market fears of further rate hikes which naturally saw us climb to the higher market prices we see now.

Last week, we just received confirmation of the April 2024 CPI data, of which the markets were pricing in at 3.4%, which unlike the last few months forecasts for inflation, we in-fact achieved this month around, further solidifying in the minds of market participants that the FED’s fight against inflation may be nearing a conclusion. This overall risk- on sentiment has historically trickled down from US Stocks and Indices, into Cryptocurrency as the market seeks greater yields in doveish market conditions. Let’s take a deep dive into how this is impacting Bitcoin currently.

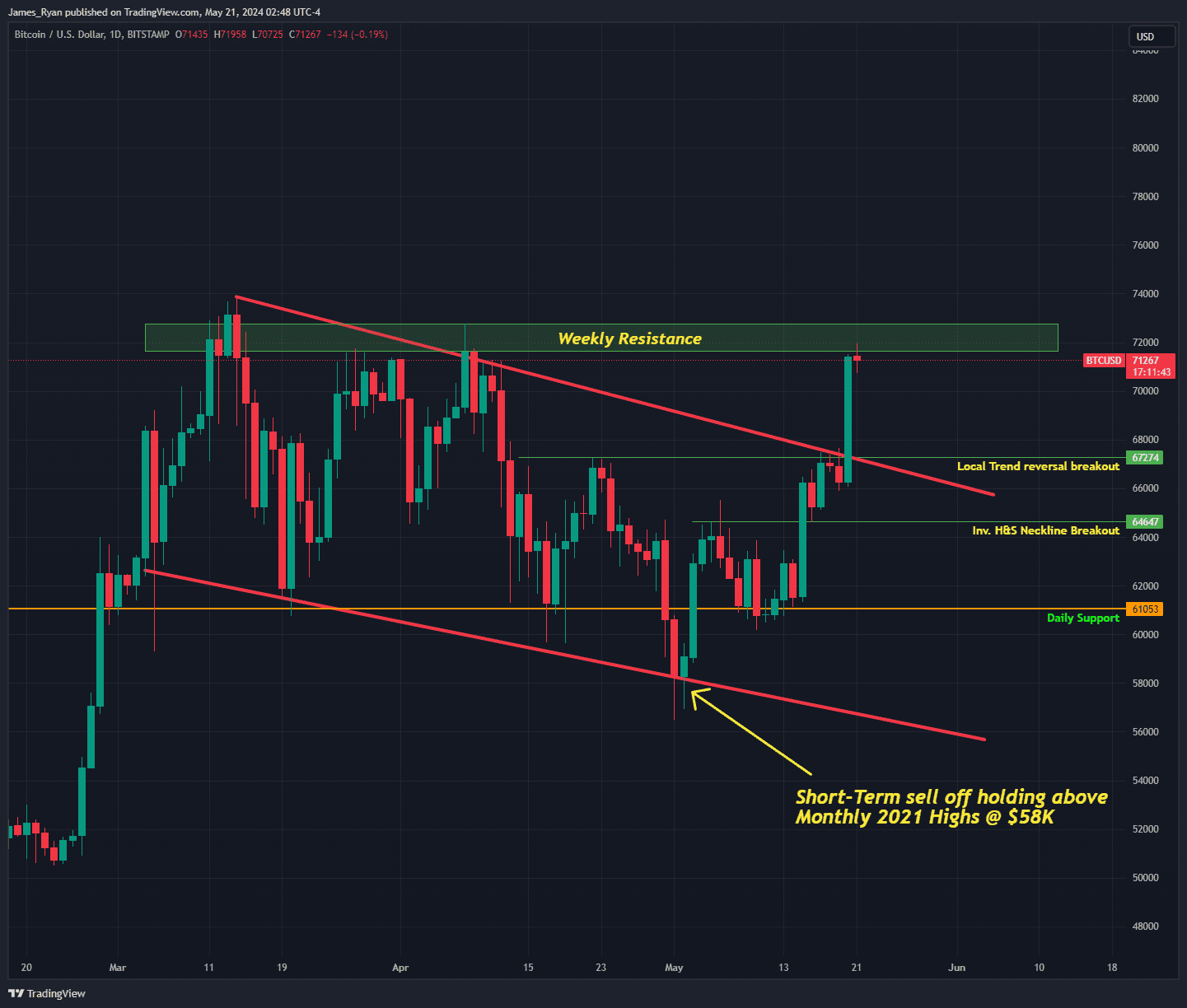

Bitcoin has seen a welcomed cooling off pre and post halving after the monstrous rally we saw in the wake of BTC ETFs, as institutional investors that were waiting on the sidelines for years to invest via the regulatory framework of traditional methods now had the means to do so. The pullback took us to a point where we quickly sold off and broke daily support at ~ $61,000, however this selling momentum wasn’t sustained with conviction on higher timeframes, ergo; allowing us to maintain price action above the 2021 Monthly highs.

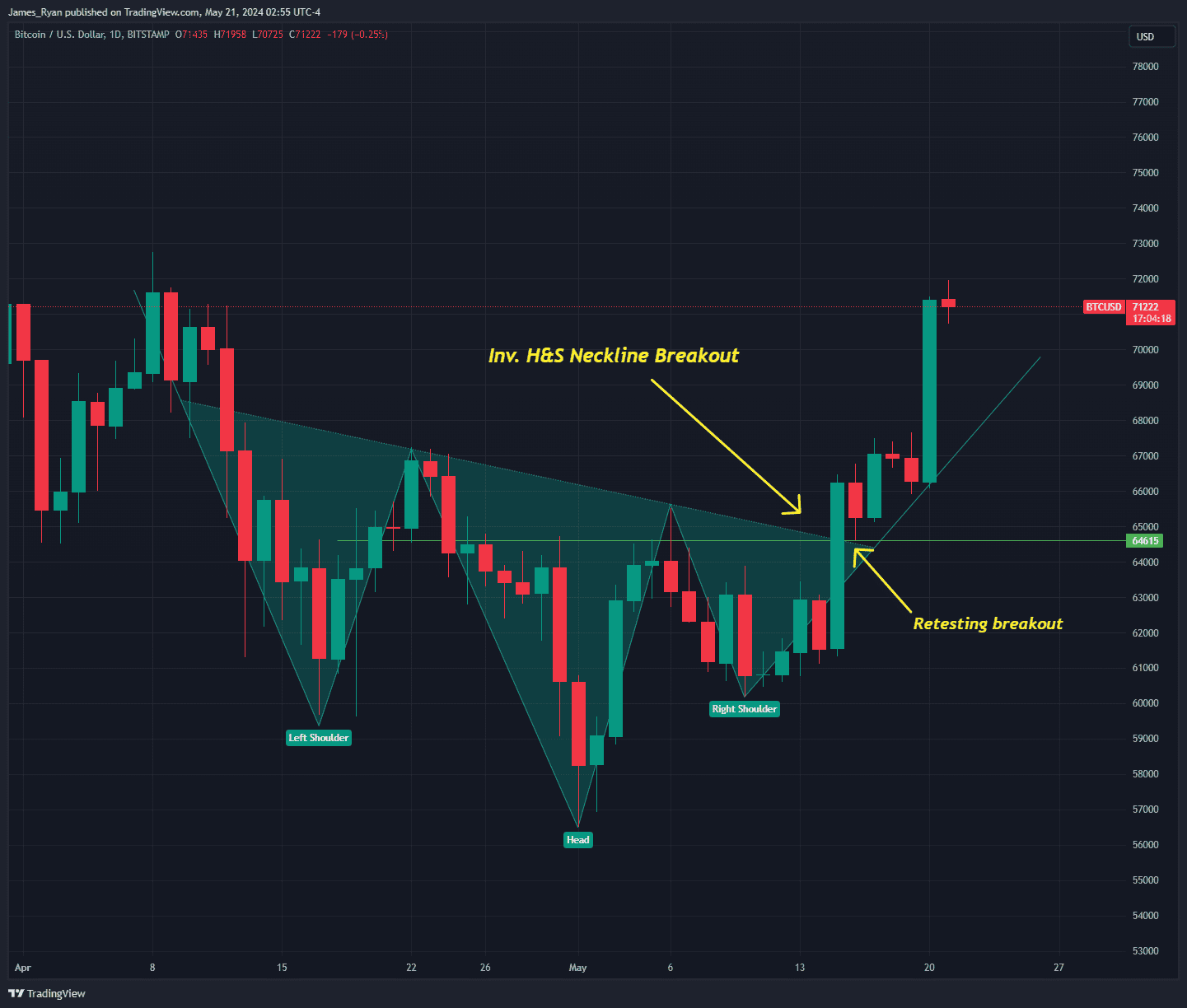

This quick sell off most likely ran the stop loss orders that we hanging around below the $61,000 Daily support zone from where price had been holding for two months prior to the capitulation, creating a slingshot back up in price. The quick regaining of this same level had then consequently set us up well for a bullish pattern, commonly seen in bull market continuations known as an “Inverse Head & Shoulders”.

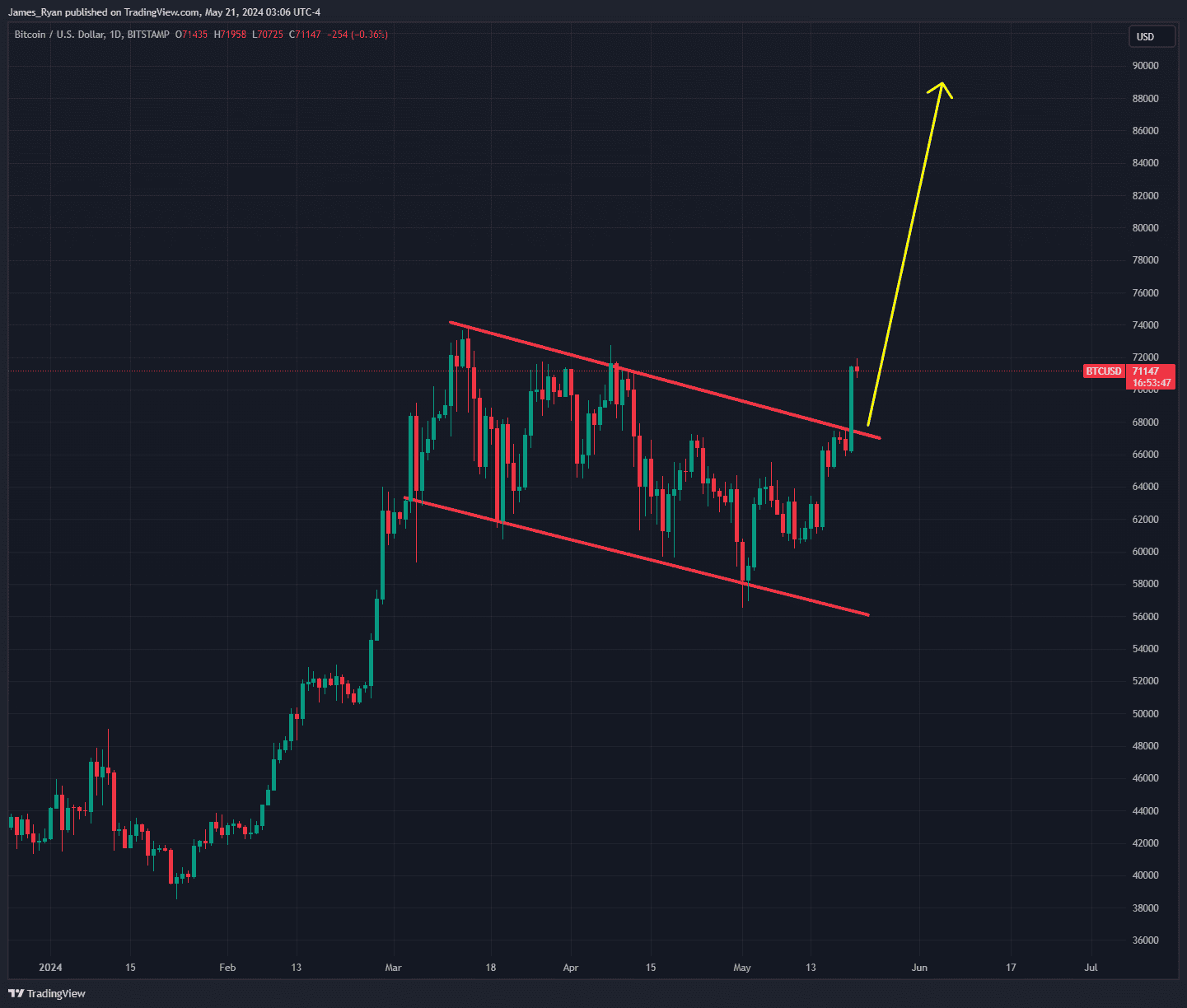

As you can see, not only did it break the neckline for this pattern, of which is the requirement to confirm the pattern itself; it also retested the breakout at $64,615, further favouring the Bulls. This combined with yet another, albeit simplistic bullish continuation pattern known as a “Bull flag” demonstrates a vast amount of technical confluence and confidence from market participants that they’re looking towards new all time highs in the near future.

As we can see, the market has responded positively to these technical setups, although a keen eye would see we are also currently at short-term resistance at the weekly highs. An ideal and healthy way the market could continue higher from here would be to retest where we reversed the local daily trend at $67,274 and continue there-after well into All-Time-High territory.

Whilst it’s needless to say it’s a good time to be a Bull right now, we also need to be aware that these are similar market conditions that preceded the sticky inflation we’ve become accustomed too in our daily lives over the last few years. It’s no coincidence that now as markets look towards new highs, we’re seeing a return of “meme investing” with an infamous figure head, under the alias “Roaring Kitty” returning to posting memes on X.com (formerly Twitter), leading a metaphorical charge and rallying his followers’ sentiments towards “Ape’ing in” to $GME (GameStop stock), such was the trend that begat the roaring 2021 Meme Stocks Bull run. As the FED was forced to fight that lagging inflation battle approximately 18-24 months after the rally by raising rates somewhat aggressively, it’s a wonder what the economic landscape might look like after this battle of steadfast bulls and ever-capitulating bears who slowly succumb to the euphoria is over possibly 18-24 months from now? Will the FED be forced to reluctantly quash market euphoria again, or in a desperate move to avoid a broader correction will they moderately maintain and even reduce rates despite rising inflation fears, proclaiming that inflation is yet again merely transitory under the guise of low unemployment and shadow statistics. Is this so called “Soft Landing” the FED are hoping to proclaim victory over in fact a doveish self-fulfilling prophecy for organic growth or a wolf in sheep’s clothing? Time will tell and here at Stormrake we’re watching with keen interest how this all plays out in the coming months ahead.

Create a brokerage account today

Reach out to us at Stormrake for further market insight and allow us to help you navigate the sea of mania and laser-eye memes, so that you can realise your goals in the market!

No Advice Warning

The information in this newsletter is general only. It should not be taken as constituting professional advice from the author - Stormrake PTY LTD.

Stormrake is not a financial adviser and does not provide financial product advice. You should consider seeking independent legal, financial, taxation or other advice to check how the information relates to your unique circumstances. Stormrake is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by this newsletter.

Disclaimer

All statements made in this newsletter are made in good faith and we believe they are accurate and reliable. Stormrake does not give any warranty as to the accuracy, reliability or completeness of information that is contained here, except insofar as any liability under statute cannot be excluded. Stormrake, its directors, employees and their representatives do not accept any liability for any error or omission in this newsletter or for any resulting loss or damage suffered by the recipient or any other person. Unless otherwise specified, copyright of information provided in this newsletter is owned by Stormrake. You may not alter or modify this information in any way, including the removal of this copyright notice.Copyright © 2024 Stormrake Pty Ltd, All rights reserved